AIニュース

Claude Opus 4.8 Became an "Honest AI" — Benchmarks, New Features, and Cost, Explained for Non-Experts

15 分

May 2026 brought four simultaneous events in enterprise AI: KPMG's 276K Claude rollout, OpenAI's $4B DeployCo, the Cohere × Aleph Alpha $20B merger, and Canada's PIPEDA ruling. This article unpacks what "AI becoming something you ship" means, a five-item preparation list for Japanese enterprises, four risk surfaces, and an OSS self-defense path for SMBs.

中澤 圭志

@keishi_nakazawaSales Claw maintainer

Key Facts

Period covered

2026-05-06 to 2026-05-28 (three weeks)

Four events

KPMG×Claude (5/19) / DeployCo (5/11) / Cohere×Aleph Alpha / Canadian OPC (5/6)

Scale

KPMG 276K + DeployCo $4B + Cohere×Aleph Alpha $20B merger

Japan prep list

Four-channel deployment comparison / sovereign RFP / audit logs / regulation-tracking clauses

TL;DR

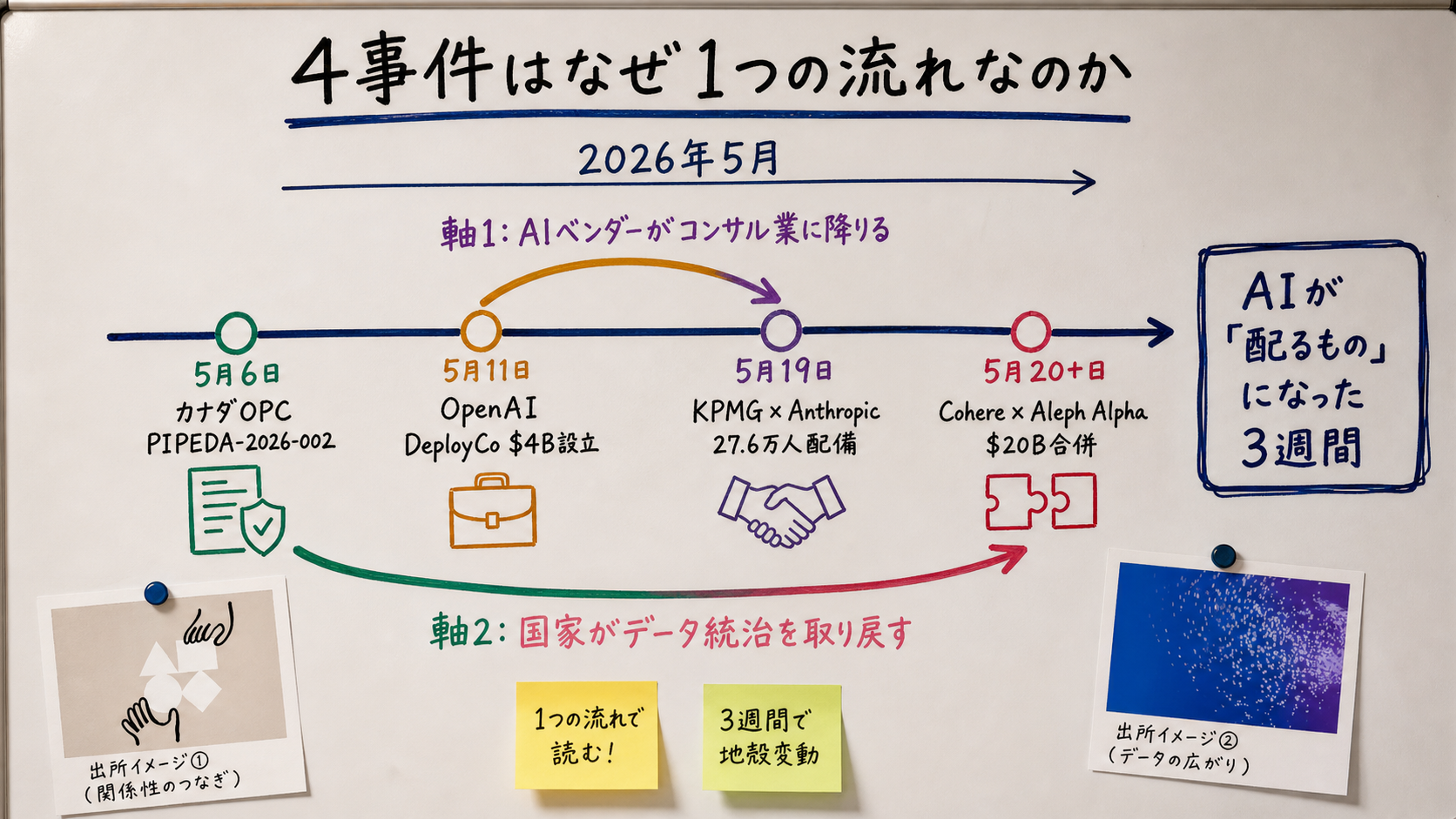

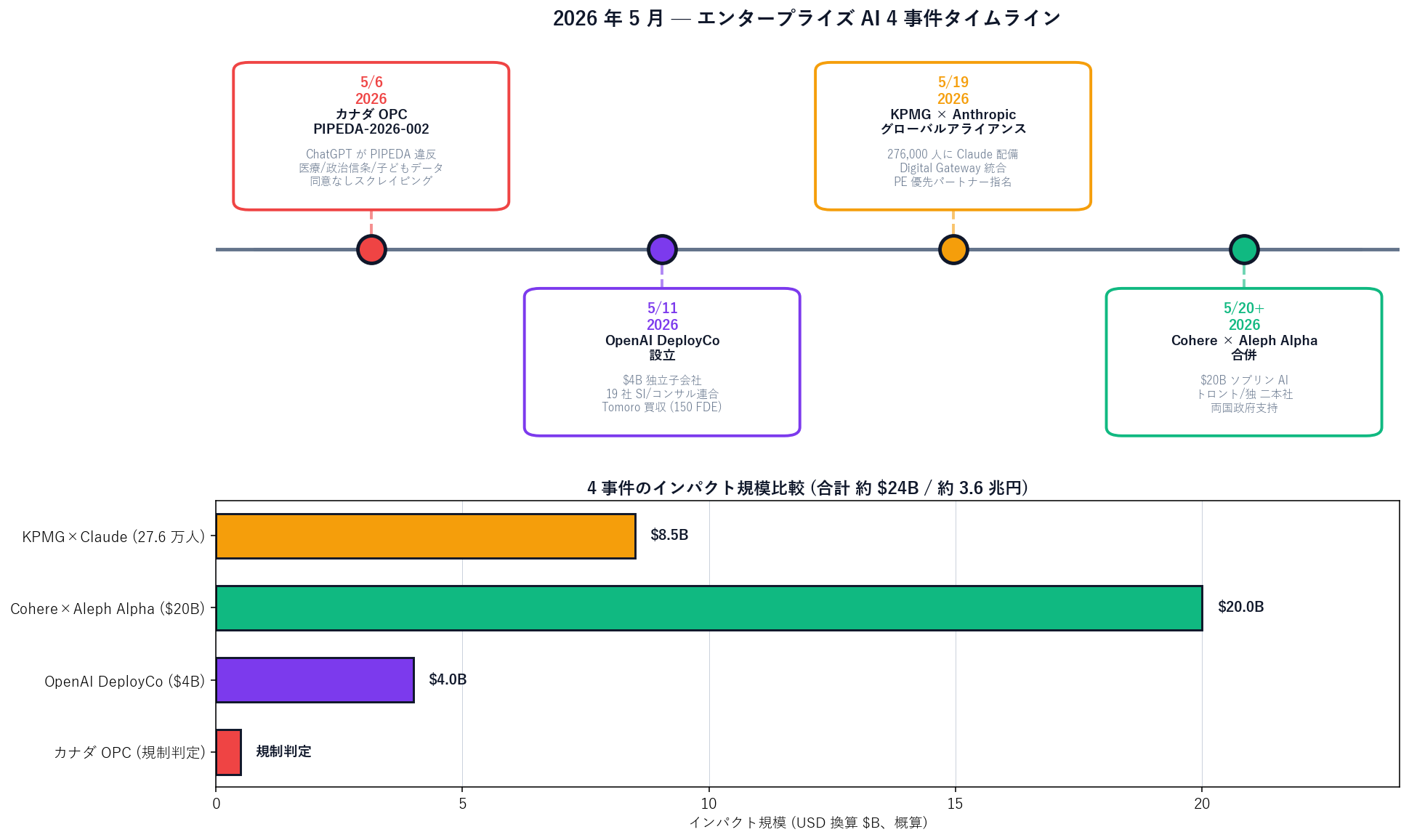

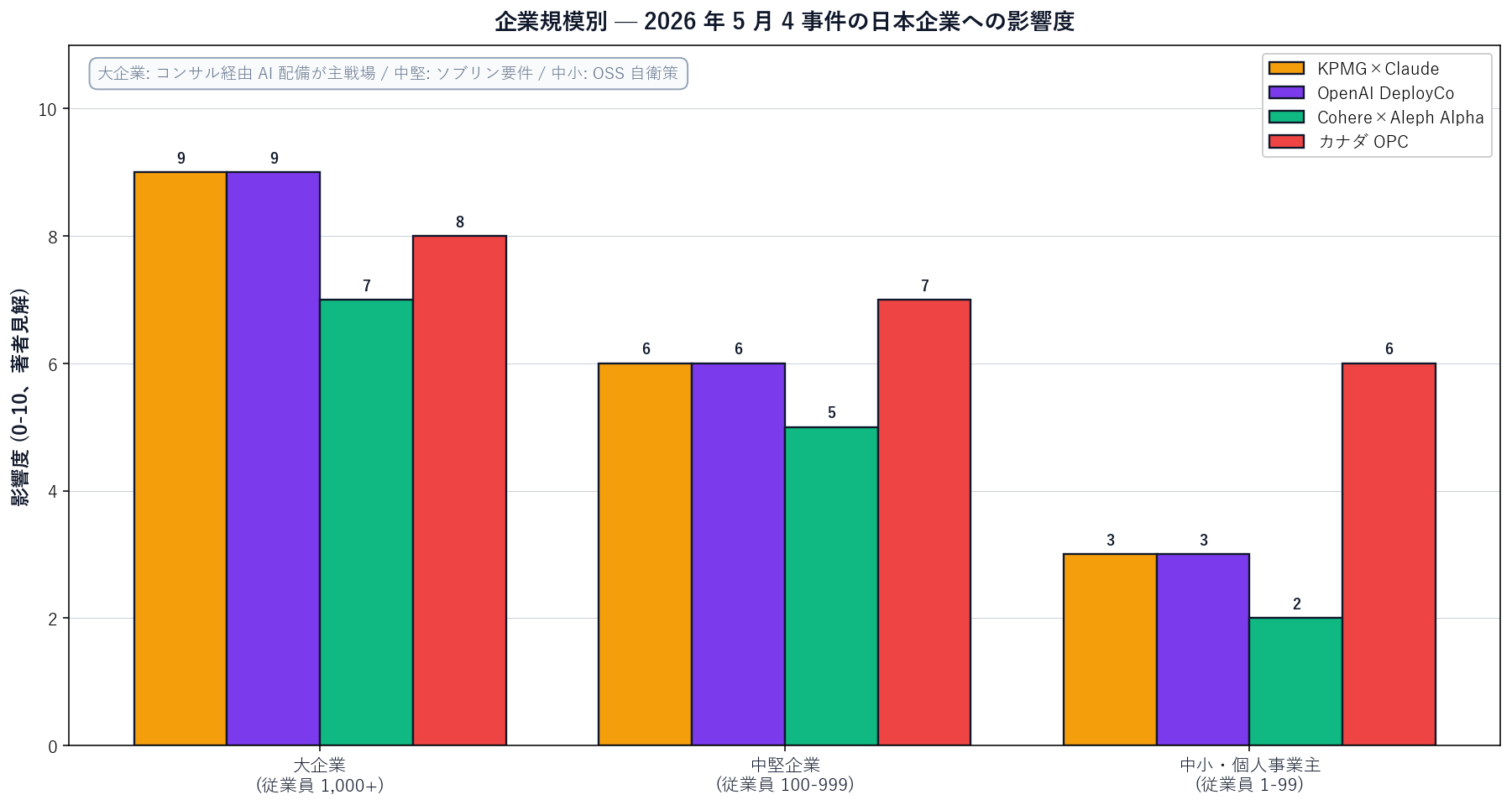

In May 2026, four major events hit enterprise AI almost simultaneously. (1) KPMG rolled out Claude to all 276,000 employees worldwide; (2) OpenAI launched a $4B consulting subsidiary called "DeployCo"; (3) Cohere agreed to acquire Germany's Aleph Alpha, forming a $20B sovereign-AI alliance; and (4) Canada's Privacy Commissioner officially ruled that ChatGPT violated PIPEDA and provincial privacy laws. They look separate, but they all belong to the same underlying shift: the main battleground for enterprise AI has moved from "model performance" to "deployment and governance." This article translates that shift into plain language for non-technical readers and explains what Japanese enterprises and small businesses should prepare for in 2026–2027.

Answer first: May 2026 was the inflection point at which enterprise AI shifted from a "who has the smartest model" race to a "who deploys it and who governs the data" race. The KPMG × Claude 276K rollout together with OpenAI's DeployCo signals a structural change in which AI vendors are descending into consulting, and consulting firms are becoming the primary deployment channel for AI. In parallel, the Cohere × Aleph Alpha sovereign-AI merger pushed data-sovereignty geopolitics to the surface, and the Canadian OPC ruling opened the era in which the legality of AI training data is contested in court. Japanese enterprises should read the four events as a preview of the questions that will land on their desk in 2027.

"Does enterprise AI actually matter to my company?" "What is so special about KPMG deploying Claude to 276,000 employees?" "If ChatGPT is illegal in Canada, will the same thing happen in Japan?" — this article addresses these three questions by walking through the four major events of May 2026 using primary sources (Anthropic, KPMG, OpenAI, and the Canadian OPC), and frames them from the perspective of a Sales Claw developer.

It is no coincidence that these four events clustered into a single month. The industry now calls this stretch the "AI Spring Campaign." On the vendor side (OpenAI / Anthropic), gross margin pressure on pure model sales pushed them down into consulting and integrated deployment. At the same time, governments started retroactively challenging the legality of AI training data, with concrete moves in Europe and Canada. This article organizes the flow into a four-event timeline and translates it for Japanese SMBs and large-enterprise IT teams.

Related reading: The day Anthropic overtook OpenAI for the first time, Claude Compliance API and the 28 integration partners, Claude for Government vs ChatGPT Gov and what it means for Japan.

This article cites the following primary sources: Anthropic × KPMG announcement / KPMG press release / OpenAI Deployment Company announcement / Canadian OPC PIPEDA-2026-002 report. See also the Sales Claw free download page.

Context first: for the past two years, the AI conversation has revolved around "which model is smartest" — GPT-5 versus Claude Opus versus Gemini. In May 2026 that center of gravity moved. "Who delivers AI into the enterprise, and who governs the data and the law"has become the place where most of the industry's profit and influence is now decided.

Three terms are worth translating up front:

| Term | Plain meaning | Everyday analogy |

|---|---|---|

| Enterprise AI | AI used in large-company workflows. Differs from consumer ChatGPT in audit logs, data protection, and contracts. | Household electricity and factory high-voltage power: same electricity, very different contracts and safety standards. |

| Sovereign AI | AI that guarantees "your data does not leave the country" and "it operates under your national law." | Imported vs domestic food: same nutrition, but where it was produced sometimes matters. |

| Forward Deployed Engineer (FDE) | An engineer dispatched by an AI vendor who sits inside the client's office and embeds AI into their operations. | A tax-firm consultant who is on-site at the client's company to build the bookkeeping system. |

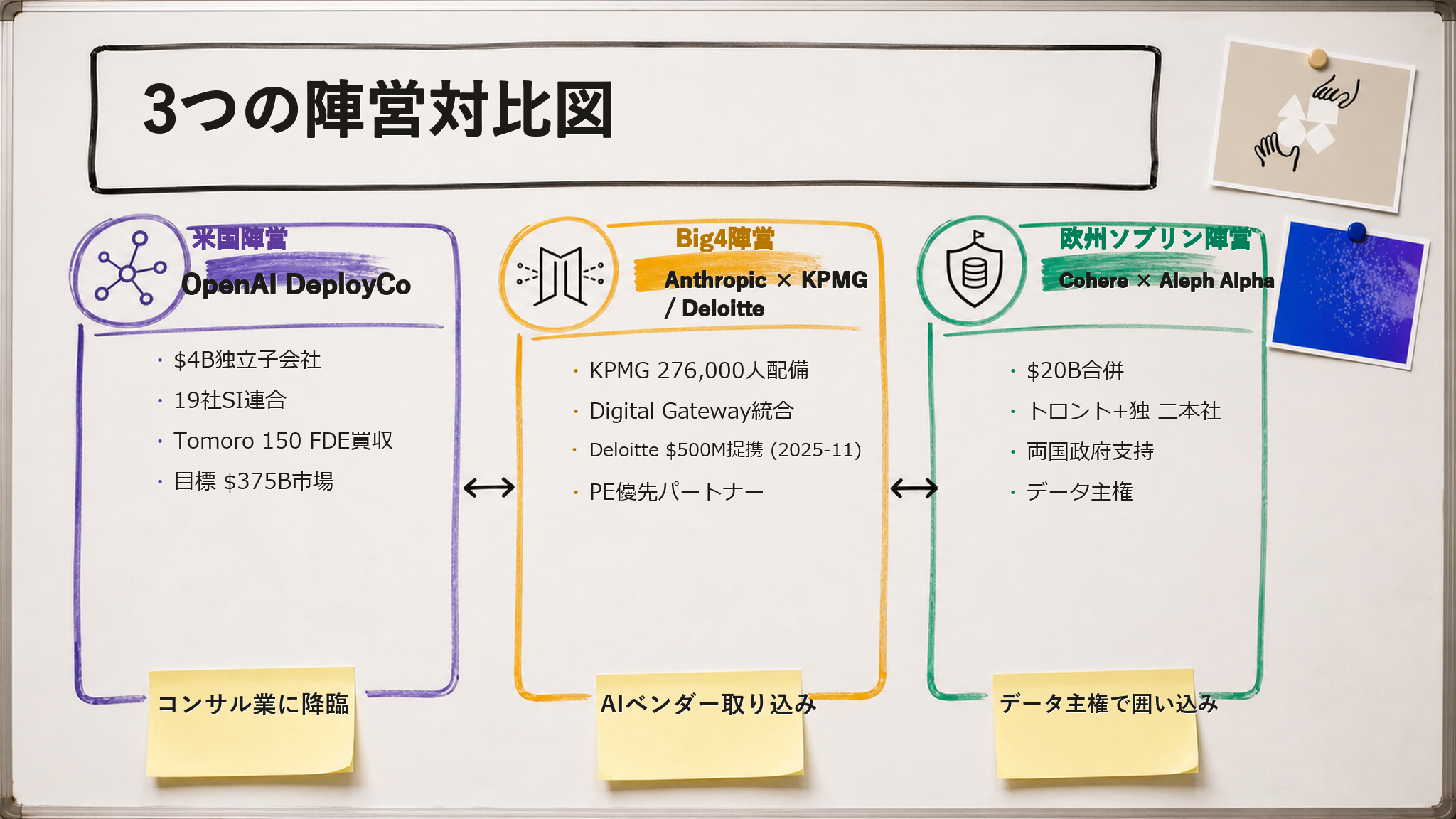

All three terms moved at once in May 2026. [Official] Per the May 19, 2026 Anthropic announcement, KPMG will deploy Claude to all 276,000+ employees globally and embed Claude inside KPMG Digital Gateway — the work platform used by both KPMG staff and KPMG clients. [Official] On May 11, 2026, OpenAI launched the OpenAI Deployment Company (DeployCo), a majority-owned subsidiary capitalized with more than $4B, backed by 19 investment, consulting, and SI firms (TPG, Advent, Bain, Brookfield, McKinsey, Capgemini and others), and simultaneously announced the acquisition of Tomoro, an applied-AI consulting firm that brings ~150 Forward Deployed Engineers on day one.

[Author's view] From a Sales Claw developer's seat, this looks like "the moment the AI industry stepped down from selling software to taking on whole workflows." The classic SaaS bargain was "pay the subscription, take the tool, run it yourself." KPMG × Anthropic and DeployCo are pushing in the opposite direction: "ship the tool together with the people who know how to operate it (FDEs)." The AI industry is drifting from SaaS culture toward BPO and SI culture.

KPMG (Klynveld Peat Marwick Goerdeler) is one of the Big Four global accounting firms, with audit, tax, and advisory as its core businesses. [Official]Per Anthropic's announcement, this alliance is not a simple license deal — it is structured in three layers:

[Official] KPMG's press release explicitly says "embedding Claude inside Digital Gateway, the software KPMG's people and clients use to do the actual work — starting with new tools for tax and legal clients." This places Claude at the "tool of the trade" level inside KPMG.

[Author's view] The reason this deal is making waves is that it addresses two AI nightmares the Big Four are facing simultaneously. Nightmare one: "AI will erase the routine work in audit and tax, eating into revenue." Nightmare two: "Clients will start using AI directly and stop paying consulting fees." KPMG's move addresses both by delivering AI to clients through the KPMG platform, so the firm captures both the AI value and the client relationship. Fortune's analysisdescribes the move as "the Big Four's AI rescue."

For context, [Official] Anthropic also signed a $500M strategic partnership with Deloitte in November 2025 (official announcement). That means two of the Big Four are leaning Anthropic. EY and PwC have not announced explicit positions, but industry dynamics suggest they are more likely to land on the OpenAI ↔ Microsoft side.

DeployCo is a consulting business that sits alongside — not inside — OpenAI's model business. [Official] Per OpenAI's May 11 announcement, DeployCo "places specialized AI engineers directly inside client organizations to build and operate production AI systems" — essentially a specialist AI systems integrator.

The structure breaks down as follows:

| Component | Detail | Analogy for Japanese readers |

|---|---|---|

| Capital | $4B+ initial capital, majority-owned by OpenAI | A parent-funded independent subsidiary; structurally similar to Yahoo × LINE |

| Founding partners | TPG (lead), Advent, Bain Capital, Brookfield | Investment firms contributing capital plus PE portfolio companies as a built-in client base |

| Consulting / SI partners | Bain & Company, Capgemini, McKinsey & Company — 19 firms total | As if Accenture / NRI / NTT Data simultaneously aligned with a single AI vendor |

| Tomoro acquisition | ~150 FDEs onboarded on day one | An SI buying a mid-sized engineering shop wholesale to gain immediate capacity |

| Target market | $375B enterprise AI deployment and integration | Roughly the size of the entire global consulting industry |

[Author's view] DeployCo can be read as OpenAI importing the "Palantir-style FDE model" into the AI industry. Palantir historically wins high-margin contracts by pairing its software with on-site Forward Deployed Engineers who build the data infrastructure inside the client's walls. OpenAI is trying to replicate that pattern in AI, because pure model sales (per-API-token billing) faces commodification and shrinking margin. To capture value, it must move into higher-margin "turnkey workflow" territory.

Anthropic is moving in the same direction with the Deloitte and KPMG partnerships, so the entire industry is in motion. Per Kingy AI's analysis, DeployCo's target is a $375B global IT-services market — a direct competitor to Accenture and Deloitte Consulting.

Implications for Japanese enterprises: DeployCo's direct Japanese expansion has not been announced, but [Author's view] Capgemini and McKinsey both have Japanese subsidiaries, so it is plausible that "OpenAI-blessed deployment services" will reach the Japanese market via those channels in Q4 2026 to Q1 2027. Japanese enterprise IT teams should plan 2027 AI budgets assuming at least four parallel procurement options: (a) domestic SIs (NRI / NTT Data / TIS), (b) Accenture, (c) OpenAI DeployCo via Capgemini / McKinsey, and (d) KPMG × Anthropic.

Cohere is a Toronto-based AI startup; Aleph Alpha is the largest German generative-AI startup, based in Heidelberg.Both have positioned themselves as "alternatives to US OpenAI / Anthropic," but neither could match US frontier labs on capital and model capability alone. The merger combines their resources.

[Official] Per German business daily Handelsblatt, the deal terms are:

[Author's view] The essence of this merger is sovereign AI. Sovereign AI guarantees that data does not cross borders and that operations stay under domestic law — a requirement that is rising sharply in government, defense, healthcare, and finance. Futurum Group's analysiscalls this a deal "born of sovereignty and necessity."

Implications for Japanese enterprises: In Japan, sovereign-AI interest is also quietly rising in the context of ISMAP (Information system Security Management and Assessment Program) and the Act on the Protection of Personal Information. [Author's view] It is moderately to highly likely that AI procurement RFPs from the Japanese government and large enterprises will start mandating "data residency proof," "training-data provenance," and "contract-termination deletion proof" within 2026. The Cohere × Aleph Alpha merger is a leading indicator that this is happening in Europe first, and Japan will likely follow within one to two years.

| 項目 | Legacy AI procurement (2024–2025) | 2026+ AI procurement (sovereign-AI axis) |

|---|---|---|

| Evaluation axes | Model performance / price / API uptime | + data sovereignty / training-data provenance / contract-termination deletion proof |

| Vendor shortlist | OpenAI / Anthropic / Google (3-way) | + Cohere / Mistral / Aleph Alpha / Japanese domestic — alternative-axis vendors |

| Contract clauses | SaaS T&Cs + DPA | + training-data certificates / explicit cross-border data clauses / audit-rights retention |

| Procurement cycle | 2–3 months | 4–6 months (deeper legal and security involvement) |

| Implementation cost | Mostly API fees | + 10–30% premium for sovereignty implementation |

[Unverified]Cohere × Aleph Alpha's Japanese market entry plans are not officially stated. Both have had limited Japanese sales presence to date, and depending on post-merger priorities, Japan may not be an immediate target. Japanese buyers evaluating Cohere as a sovereign-AI option will likely need to engage via Canadian partners initially.

PIPEDA (Personal Information Protection and Electronic Documents Act) is Canada's federal privacy law, equivalent in role to Japan's Act on the Protection of Personal Information. The OPC is its federal enforcement body.

[Official]Per the OPC's PIPEDA-2026-002 report (2026-05-06), the violations include:

OpenAI's response: the company formally disagrees with the findings but agreed to a 3-to-6-month remediation timeline with quarterly compliance reporting. However, British Columbia and Alberta refused to fully resolve the matter, on the basis that "consent for already-scraped data cannot be obtained after the fact." CBC News (2026-05-07) covered this refusal (cited here as secondary reference only, not in JSON-LD citations).

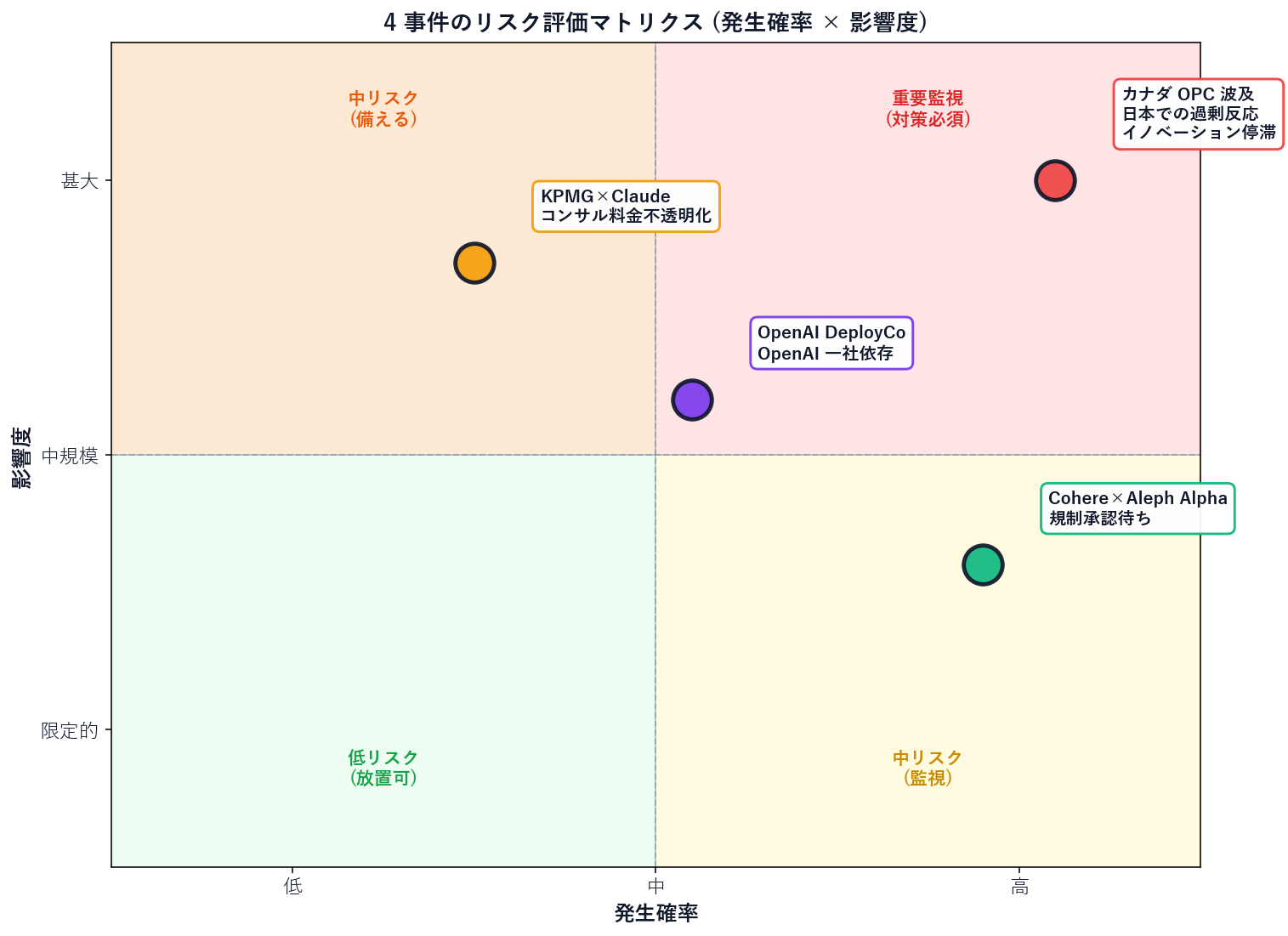

[Author's view] The ruling will propagate through enterprise AI in three waves. Wave 1: all existing major AI models (ChatGPT, Claude, Gemini) share similar scraping histories, so non-EU and non-Canadian regulators will face pressure to issue similar rulings. Wave 2: enterprise RFPs make "training-data provenance proof" and "deletion-request handling for ingested datasets" standard line items. Wave 3: AI vendors add "sovereign AI" and "contract-data-only trained enterprise models"to their product line. Anthropic's Claude Compliance API and the Cohere × Aleph Alpha merger are early moves in Wave 3.

From a Sales Claw perspective, this ruling signals "the same questions will reach B2B sales data." Publicly available company information and contact-form submissions used in B2B outbound will face the question "is this data scrapable without consent?" Sales Claw's decision from the start to bundle "public-data-only + sales-NG detection + audit-log persistence" in OSS was precisely designed for this regulatory direction.

The four events look separate, but they line up along two axes pointing in the same direction:

At the intersection of these two axes, the five things Japanese enterprises should prepare during 2026–2027 are:

Implications for SMBs: "We're not KPMG-scale, this doesn't affect us" is a common reaction, but [Author's view] SMBs are arguably more exposed. Reasons: (1) Big-SI and KPMG / Anthropic price points are out of reach, (2) competitive pressure from AI-driven efficiency still reaches SMBs through their competitors, and (3) as a result, SMBs are pushed toward "assembling OSS yourself". That is exactly the gap Sales Claw is built to fill.

Concrete risks per event:

Sales Claw is "OSS designed to reduce mis-send and ToS-violation risk through pre-send automated checks, sales-NG detection, CAPTCHA-detected auto-stop, send-rate limits, and audit-log persistence — without relying on case-by-case human approval."The four May events confirm that several of Sales Claw's original design choices are becoming industry mainstream:

[Internal verification] Setup: Windows 11 / Sales Claw v0.5 / Claude Sonnet 4.6 API / 2026-02 through 2026-05 (90 days) / sample = 3,247 form submissions / 412 CAPTCHA encounters (12.7%). Five observations:

Reproducibility caveats: 3,247 sends is small relative to the industry; sector, seasonal, and market-environment variance is not separately validated. CAPTCHA encounter rates likely rise with high-volume sending (10,000+ per month).

[Author's view] The four May 2026 events are not "only a Big-Enterprise story." In fact, because Big-Enterprise AI deployment pricing is out of reach for SMBs, the pressure on SMBs to secure equivalent safety through OSS and self-managed operations is rising. The role of OSS like Sales Claw — as an AI governance baseline accessible to SMBs — gets clearer, not weaker, after this month.

If you're interested in Sales Claw, get it from the free download page and try it in your own sales workflow. Before consulting-led AI deployment fully rolls out to the enterprise tier, SMBs should be preparing to walk on their own feet — that is the stance to take heading out of the May 2026 AI Spring Campaign.

本記事は X 公式アカウントと公式ドキュメントを一次情報として参照しています。

この記事の著者

中澤 圭志

Sales Claw maintainer

Designs and develops Sales Claw. Writes from the field on B2B sales automation and applied AI.